What you'll learn 👉

Best crypto tax software in Australia

Crypto taxes are complex and you have to pay them if you’re living in Australia.

You might want to keep your digital currency holdings separate from your regular investments, but you still need to pay income tax like everyone else. If you’re looking for a way to simplify your tax reporting, i.e., report them to the ATO, there are plenty of crypto tax software programs out there. But which one do you choose?

We’ve put together a list of the best crypto tax calculators for Australian taxpayers.

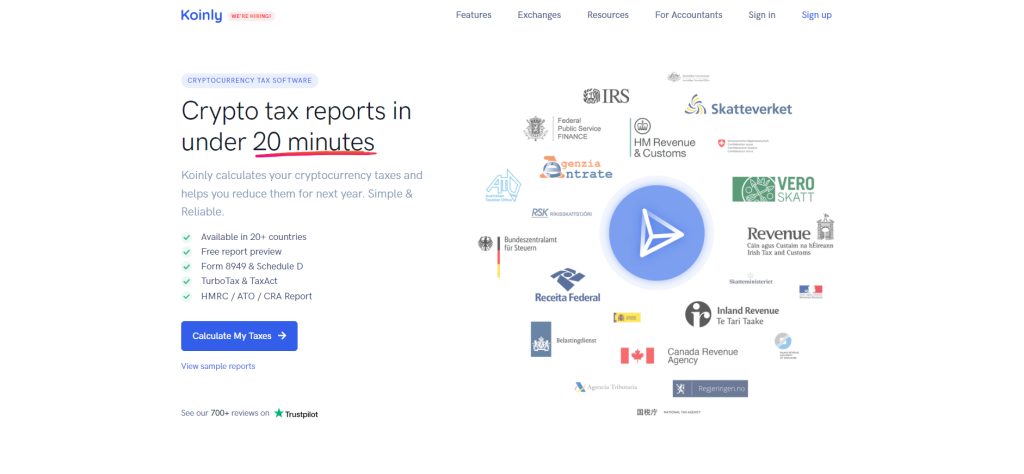

Best for ease of use: Koinly

Koinly is one of the most popular crypto tax reporting apps out there. It lets people easily generate tax reports in just about 20 minutes and supports data import from over 400 crypto exchanges and over 100 crypto wallets, and it provides auto-syncing of your transaction data.

The app is specially designed for Australians and others living outside the US, UK, and Canada. Its unique tax report templates are tailored specifically for Australian taxpayers, including how much income you earned and what deductions you can make. It even generates a full-fledged PDF file for filing purposes.

Also, Koinly says they support NFTs, but if you look into it, they put all costs of NFTs zero. Please be aware of this.

Koinly is free to use to calculate gains, track transactions etc. However, the tax reports are priced depending on the amount of transactions, up to 100 transactions is $49 and the more transactions you have, the more you pay (up to $279 per year).

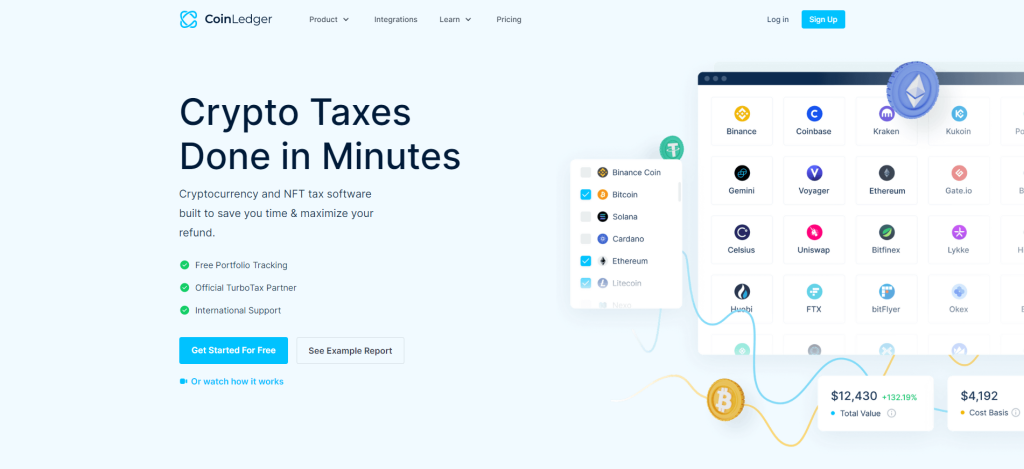

Best for tax professionals: Coinledger

CoinLedger is a crypto tax calculator first launched in the United States only. It’s now a global tax reporting system that may be used in any country that recognizes FIFO, HIFO, or LIFO accounting, including Australia.

As a result of its straightforward design, over 300,000 crypto investors are currently using this crypto tax software. They’re compatible with numerous exchanges, wallets, NFTs, Defi, and over 10,000 other cryptos.

It’s simple to import your past transactions because it syncs directly with your preferred platforms. You may easily import your transactions and calculate your taxes, whether you are a trader, earn interest, or purchase NFTs.

It does not offer a free pricing plan. Annual subscriptions range in price from $49 to $299, depending on the number of transactions it provides.

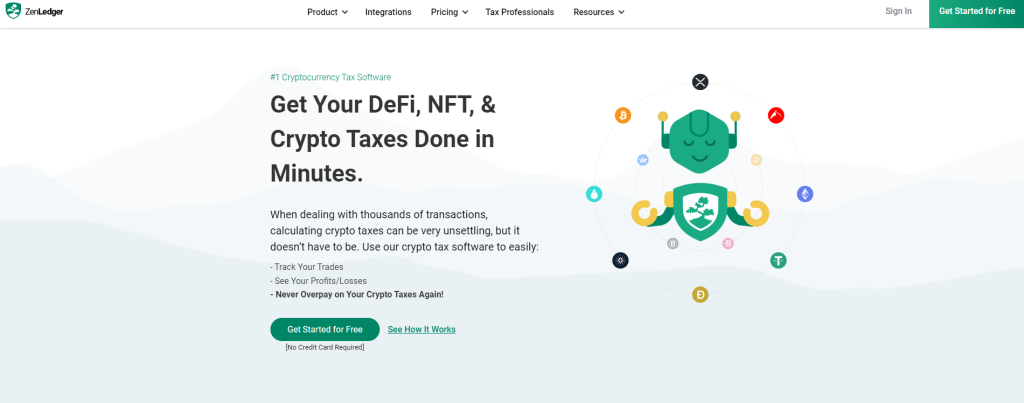

Best for DeFi & NFTs: ZenLedger

ZenLedger is one of the most popular crypto tax software platforms. With its easy-to-use interface, it is designed to help people easily manage their crypto transactions and file their taxes efficiently.

The process is straightforward. Simply import your transaction history, check the information, and download the form. Zenledger is trying to separate itself from the competition by offering a distinct DeFi tool which supports more than 30 distinct De-Fi protocols. Aside of that, Zenledger integrates with well over 400+ exchanges and wallets.

The exceptional quality of ZenLedger’s customer service is another element that stands out. Its professionals are reachable by chat, email, and phone calls around the clock, every day of the week.

The platform has a free pricing plan, limiting up to 25 transactions. Annual subscriptions range in price from $49 to $999, depending on the number of transactions it provides.

Best for most supported exchanges: Coinpanda [AVOID!]

Climbing up the ranks of top crypto tax calculators in recent years is Coinpanda. It’s available for users in over 65 countries and has over 40,000 satisfied users. More than 500 crypto exchanges and wallets, as well as other blockchains, are supported by the program.

In fewer than 20 minutes, you can get a complete crypto tax report.

Aside from that, it can also be used as a portfolio tracker to keep tabs on your investments and take advantage of tax deductions for coins and investments that recorded a loss. Users may monitor their crypto holdings, gain insight into profitable trades, and minimize their tax liability all in one place.

The platform has a free pricing plan, limiting up to 25 transactions. Annual subscriptions range in price from $49 to $189, depending on the number of transactions it provides.

Best free plan: CoinTracking

With the help of CoinTracking, you can simply prepare tax reports in real-time and analyze your trades. It generates tax reports that include information about the entire value of your coins as well as their gains, losses, and profits—realized and unrealized.

No matter if you’ve only recently begun investing in cryptos or have been doing so profitably for a while, it enables you to keep track of your transactions in real-time. In a word, automation helps to reduce the amount of paperwork needed.

Each trader’s transactions are instantly downloaded into the tax software from their exchanges. Then it creates brief, precise tax records that express the amount owed in crystal clear detail.

The platform has a free pricing plan, limiting up to 200 transactions. Annual subscriptions range in price from $10.99 to $54.99 per month (billed annually), depending on the number of transactions it needs to process.

Best for high-volume traders: Cryptotaxcalculator

Cryptotaxcalculator is Aussie based and preferred by patriots. It is tailored to the needs of ordinary taxpayers but also accountants and bookkeepers, and it includes support for tax regulations in Australia and around the world. This makes it perfect for accountants and anyone else who wants to keep tabs on their crypto holdings.

The tool can produce tax reports for more than 20 nations and it has processed more than 150 million transactions for more than 100,000 users to date.

It examines the addresses of your digital wallets and generates reports mechanically based on your transaction history. The information can be exported to a CSV file, or a PDF document can be generated without leaving the app.

It does not offer a free pricing plan. Annual subscriptions range in price from $49 to $299, depending on the number of transactions it provides.

How is crypto taxed in Australia?

As far as the Australian government is concerned, Bitcoin and other cryptos are neither money nor foreign currency. The ATO instead considers bitcoin to be property. Coins, tokens, NFTs, and stablecoins all fall under this category.

However, depending on the circumstances of the exchange, crypto may potentially be considered taxable income. It all comes down to your individual situation and the nature of the transactions you engage in to determine how much tax you owe.

Capital Gains Tax (CGT) on crypto

When you trade cryptos, you must be aware of Capital Gains Tax. Selling doesn’t just refer to selling a coin for fiat currency. It includes any transaction where you’re trading ownership of one crypto. This include:

- Giving crypto as a gift.

- Swapping one crypto for another, including stablecoins and NFTs.

- Selling crypto for AUD or another fiat currency.

- Buying goods and services with crypto (if not seen as a personal use asset).

Capital gains taxes can be reduced by half if crypto is held for at least a year before being sold.

Capital Gains Tax rate

The net capital gain from the sale, exchange, consumption, or gifting of crypto by an individual is subject to taxation at their applicable Income Tax rate. Your total income for the tax year determines your income tax rate.

ATO Individual Income Tax Rates

According to your circumstances, these income tax rates illustrate the amount of tax payable in every dollar for each income tax bracket. People who are considered permanent residents of Australia are subject to these tax rates.

| Taxable income | Tax on this income |

| 0 – $18,200 | Nil |

| $18,201 – $45,000 | 19 cents for each $1 over $18,200 |

| $45,001 – $120,000 | $5,092 plus 32.5 cents for each $1 over $45,000 |

| $120,001 – $180,000 | $29,467 plus 37 cents for each $1 over $120,000 |

| $180,001 and over | $51,667 plus 45 cents for each $1 over $180,000 |

*The 2% Medicare surcharge is not reflected in the above prices.

How to calculate crypto capital gains?

The profit you make when selling or otherwise getting rid of your crypto is the difference in price between when you bought it and when you sold it. The appreciation in the value of your crypto has resulted in a capital gain, which is subject to Capital Gains Tax.

Simply put, your cost basis is the total amount you spent on buying the crypto and any associated fees. Your crypto sale price should be reduced by its cost base.

If you sold, gave away, or otherwise disposed of crypto, deduct its cost basis from its fair market value in AUD on the day of disposal.

Crypto capital losses

When selling crypto, if your earnings are less than your initial investment, you incur a loss.

In the event of a capital loss, the amount of the loss can be offset against capital gains or carried forward to subsequent years. Capital losses can be carried over indefinitely, but they must be utilized when first becoming available.

No net capital loss can be offset by other types of revenue.

Crypto wash sale

The term “wash sale” refers to the practice of quickly selling and buying the same or similar asset (such as crypto) again. A wash sale occurs when taxpayers intentionally generate a loss to reduce their taxable income.

There may be an additional tax, interest, and penalties for taxpayers who engage in wash sales, as stated by the ATO.

Crypto tax breaks

The Australian tax system provides its citizens with a range of tax-free levels and allowances that can be used with crypto.

One of these is once your annual income surpasses $18,200, you will be required to start paying income tax. Also, individuals may be eligible for a 50% CGT deduction if they hold crypto for more than a year before selling or exchanging it.

If you own cryptos for your own use, you may be able to avoid paying capital gains tax on your investment. Assets acquired for less than $10,000 in crypto and used to immediately acquire another asset for personal use or consumption fall under the umbrella term “personal use assets.”

Tax on lost or stolen crypto

A capital loss may be claimed in the event of the loss of a private key or the theft of crypto, depending on the circumstances. It all comes down to proof—proof of loss and proof that you won’t be able to get your funds back.

Income Tax on crypto

In some instances, crypto is considered income and must be taxed as such, rather than being subject to Capital Gains. Income tax is due on crypto gains from:

- Getting paid in crypto

- Airdrops

- Staking rewards

- Referral bonus

- Defi Interest

Tax-free crypto

In Australia, some crypto-related operations may fall under the tax-exempt category. When dealing with DeFi transactions or straddling the line between “investor” and “trader,” the lines between taxable and tax-free activity can become muddled rapidly.

For the following scenarios, crypto taxes will not be charged:

- Buying crypto with AUD

- Holding crypto

- Mining crypto – at a hobby level

- Donating crypto to charity

- Under $10,000 crypto purchases (crypto for personal use asset)

- Shifting crypto between wallets (watch out for transfer fees)

Tax on buying crypto

There is none.

AUD crypto purchases are tax-free in Australia. When you sell or “dispose” of your crypto, you must pay tax.

If you acquire and hold crypto, you won’t owe tax even if your portfolio’s value rises. Selling, exchanging, or gifting crypto is taxable.

In Australia, exchange crypto is taxable. Australian tax legislation requires crypto sales to be paid in Australian dollars. Capital gain is determined using the market value of the purchased coins (in AUD). If the crypto you got can’t be valued, use the market value of the crypto you sold during the transaction.

Tax on selling crypto

Your level of patience will determine the outcome.

ATO states that the sale of crypto for a fiat currency such as the AUD constitutes a taxable event. Also, the sale, swap, or trade of one crypto for another is a taxable event subject to Capital Gains Tax, much like the purchase of one crypto with another.

If you hold crypto for a minimum of a year, you will pay 50% less tax.

Tax on staking, mining, airdrops, NFTs, DeFi

Any income earned from Staking rewards will constitute an Income tax equal to the money value of the tokens they receive.

If you are a hobby miner, your mined coins are not income but rather a capital acquisition, and it is tax-free until their disposal when they are subject to capital gain tax.

Any airdrops you receive are counted as regular income at the tokens’ fair market value on the day you got them. Your airdropped coins or tokens will be handled as a typical capital gains event if you sell, trade, spend, or gift them.

If you are a trader, you pay Income tax when you create, sell, or farm NFTs for a staking reward. If you are not a trader, you pay Capital Gain Tax when you buy an NFT with crypto, sell an NFT for crypto or fiat currency or swap an NFT for another NFT.

With DeFi, if you earn new coins or tokens as a result of your transactions, you will pay Income Tax. If you swap, sell or spend tokens on DeFi platforms, you will pay Capital Gains Tax.

Read also:

- How To Do Your Kraken Taxes?

- How To Do Your Trust Wallet Taxes?

- Best Crypto Tax Software in Canada

- Borrow against crypto to avoid taxes

- How to pay taxes on DeFi

FAQs

Your crypto investment is typically subject to capital gains tax in Australia. When filing your income tax return, you must disclose all capital gains and losses and pay income tax on any net gains.

Yes, Koinly is good for Australia, it assists you in determining your capital gains in conformity with the ATO’s regulations.

No, CoinSpot does not give the ATO a tax report.

HODLing is one method of lowering this taxation. A 50% long-term capital gains tax discount is available to Australian investors who retain assets for more than a year when they sell, exchange, spend, or give them as gifts.

Yes, the ATO can see your crypto because the ATO has a crypto data-matching program running since April 2019 that gets data from share registries and crypto asset exchanges.

Yes, in order to ensure tax compliance, Swyftx, an AUSTRAC registered exchange, may share KYC data with the appropriate agencies, including the ATO.

Yes, Koinly is accepted by the ATO because it helps you calculate your capital gains in accordance with the ATO’s rules.

No, ATO has no access to KuCoin, because KuCoin does not report to the ATO because it doesn’t mandate KYC for small investors and isn’t an AUSTRAC-registered exchange.