The blockchain is a decentralized system that exists between all permitted parties. One of the best things about the blockchain is that there’s no need to pay intermediaries (Middle men) and it saves you time and conflict. Blockchains have their problems. However, they are rated, undeniably, faster, cheaper, and more secure than traditional systems. These are the reasons why banks and governments are turning to them. We can make business more efficient and make the legal system more equitable by giving computers control over contracts.

Imagine if you could make it easier to update your will, cut your mortgage rate, or ensure that your buddy was never able to weasel out of paying up on a bet? That and much more is the promise of smart contracts. Thanks to cryptocurrency smart contracts are a technology that is getting closer and closer to reality.

Smart contracts are computer programs that can automatically execute the terms of a contract and they may replace lawyers and banks for handling certain common financial transactions someday.

However, major questions abound as always with this cutting edge of financial technology: Will anyone actually use these things anyway? And, of course, how will this all align with our current legal system?

What you'll learn 👉

What are Smart Contracts?

The idea of smart contracts goes way back to 1994. That’s when Nick Szabo, a cryptographer widely credited with laying the groundwork for bitcoin, realized that the decentralized ledger could be used for smart contracts, otherwise called self-executing contracts, blockchain contracts, or digital contracts. In this format, contracts could be converted to computer code, stored and replicated on the system and supervised by the network of computers that run the blockchain and this would also result in ledger feedback such as receiving the product or service and transferring money.

Szabo’s original theories about how these contracts could work remained unrealized. The reason for this is that there was no digitally native financial system that could support programmable transactions. (If a bank still has to manually authorize the release and transfer of money the purpose of smart contracts is defeated). Phil Rapoport, Ripple Labs’ director of markets and trading says: “One big hurdle to smart contracts is that computer programs can’t really trigger payments right now.”

The advent and increasingly widespread adoption of bitcoin is changing that. As a result Szabo’s idea has seen a revival and smart contract technology is now being built on top of bitcoin and other virtual currencies.

Smart contracts help you exchange money, shares, property, or anything of value in a transparent, conflict-free way. The best thing is that smart contracts allow you avoid the services of a middleman.

Comparing the smart contracts to a vending machine is the best way to describe the technology. Usually, if you need some document you would go to a notary or a lawyer, pay them, and wait until you get the document. With smart contracts, on the other hand, you simply drop a bitcoin into the vending machine (i.e. ledger), and your driver’s license, escrow, or whatever drops into your account. This means that smart contracts define the rules and penalties around an agreement in the same way that a traditional contract does. This technology also automatically enforces those obligations.

![]()

There are currently two major open source projects working on smart contracts: Codius and Ethereum.

Codius was developed by Ripple Labs. This company also created its own digital currency called Ripple. Although Codius is managed by the private company, it aims to be interoperable between a variety of cryptocurrency, such as Ripple and bitcoin.

Ethereum is originally developed by 20-year-old programmer Vitalik Buterin. It is an entirely new currency with smart contracts baked into its payment system and it would replace other “coins” like bitcoin, but appears to be more of a community project.

Cryptocurrencies such as bitcoin are poised to help smart contracts become reality, but the effect may also be reciprocal. Smart contracts can illustrate a unique benefit of virtual currencies that some lawyers think could attract more people.

A Smart Contract Example

Suppose I rent you an apartment. This can be done through the blockchain by paying in cryptocurrency and you get a receipt. The receipt is held in our virtual contract and I give you the digital entry key which comes to you by a specified date. The blockchain releases a refund if the key doesn’t come on time. If I send the key before the rental date, the function holds it releasing both the fee and key to you and me respectively when the date arrives and, as you can see, the system works on the If-. Then premise and is witnessed by many people, which means that you can expect a faultless delivery. I’m sure to be paid if I give you the key. You receive the key if you send a certain amount in bitcoins. The document is automatically cancelled after the time, and since all participants are simultaneously alerted the code cannot be interfered by either of us without the other knowing.

Smart contracts can be used for all sorts of situations that range from credit enforcement to financial services, financial derivatives, insurance premiums, legal processes, crowd funding agreements, breach contracts and property law.

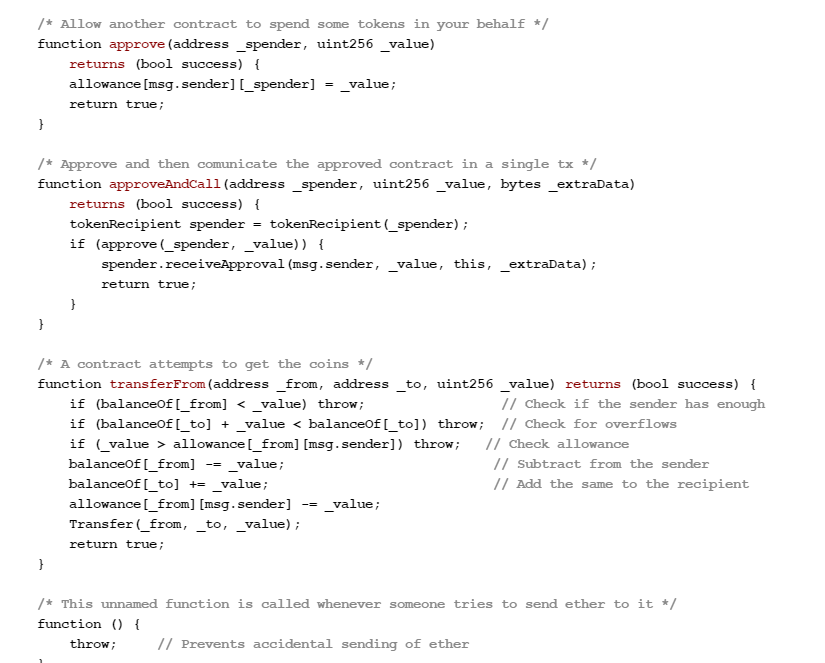

Here is the code for a basic smart contract. It was written on the Ethereum blockchain. Contracts can be encoded on any blockchain. However, Ethereum gives unlimited processing capability so it is mostly used.

An example smart contract on Ethereum. Source: www.ethereum.org/token

The contract stipulates that the creator of the contract be given 10,000 BTCS (i.e. bitcoins). It allows anyone with enough balance to distribute these BTCs to others.

Automating Simple Transactions

Let’s take a simple example, like the NBA Finals bet. Say you want to bet $500–or roughly one bitcoin–that the Cavs will win. On the other hand, your friend is betting the same amount that the Warriors will take the title. Your friend and you should place your bitcoin in a neutral account controlled by the smart contract. The smart contract would automatically deposit your bet and your winnings from your friend back into your account when the game is over and the smart contract is able to verify via ESPN, CNN, or elsewhere that the Warriors beat the Cavs.

Smart contracts are computer programs. That’s why it would be trivial to add more complex betting elements like odds and score differentials into the mix. There are services out there today that might handle this sort of transaction. However, they all charge a fee. The key difference with smart contracts is that it doesn’t require any intermediary party because it is a decentralized system accessible to anyone.

Online shopping would be a more everyday example. You might not want to pay a merchant immediately if you order something online. You will pay them when they fulfil their end of the bargain. Before releasing payment to the sender, you could easily have a contract that looks for FedEx tracking data saying that the package you ordered has been delivered to your address.

Here’s How Smart Contracts Can Be Used

Management

Because of its accuracy, transparency, and automated system the blockchain not only provides a single ledger as source of trust, but also shaves possible snarls in communication and workflow. Usually, while waiting for approvals and for internal or external issues to sort themselves out, business operations have to endure a back-and forth. A blockchain ledger streamlines this and it also cuts out discrepancies that typically occur with independent processing. This may lead to costly lawsuits and settlement delays.

Government

Insiders vouch that it is extremely difficult for our voting system to be rigged. However, smart contracts would allay all concerns by providing an infinitely more secure system. Ledger-protected votes would need to be decoded and require excessive computing power to access but no one has that much computing power. Furthermore, smart contracts could hike low voter turnout. Much of the inertia comes from a fumbling system. This includes lining up, showing your identity, and completing forms. Volunteers can transfer voting online with smart contracts and millennials will turn out en masse to vote for their Potus.

Case history

The Depository Trust & Clearing Corp. (DTCC) used a blockchain ledger in 2015 to process more than $1.5 quadrillion worth of securities, representing 345 million transactions.

Supply Chain

Smart contracts work on the If-Then premise. So, to put in Jeff Garzik’s words

“UPS can execute contracts that say, ‘If I receive cash on delivery at this location in a developing, emerging market, then this other [product], many, many links up the supply chain, will trigger a supplier creating a new item since the existing item was just delivered in that developing market.’” All too often, paper-based systems hamper supply chains. Here forms have to pass through numerous channels for approval and this increases exposure to loss and fraud. The blockchain provides a secure, accessible digital version to all parties on the chain to nullify this and automates tasks and payment.

Case History

Smart Contracts are used by Barclays Corporate Bank to log change of ownership and automatically transfer payments to other financial institutions upon arrival.

Real Estate

Smart contracts can get you more money. Normally, you’d need to pay a middleman such as Craigslist or a newspaper to advertise if you wanted to rent your apartment to someone. You would also need to pay someone to confirm that the person paid rent and followed through. The ledger cuts the costs. All you do is pay via bitcoin and encode your contract on the ledger, everyone sees, and you accomplish automatic fulfilment. Anyone associated with the property game, like brokers, real estate agents, hard money lenders can profit.

Automobile

We’re progressing from slothful pre-human vertebrates to super-smart robots and there is no doubt about it. Imagine a future where everything is automated and that’s where smart contracts help. The self-autonomous or self-parking vehicles are one example. Here, smart contracts could put into play a sort of ‘oracle’, the sensor or the driver, as well as countless other variables, that could detect who was at fault in a crash. An automobile insurance company could charge rates differently using smart contracts, based on where, and under which, conditions users are operating their vehicles.

Healthcare

Using a private key which would grant access only to specific individuals, personal health records could be encoded and stored on the blockchain. The same strategy could be used to ensure that research is conducted via HIPAA laws (in a secure and confidential way), which means that receipts of surgeries could be stored on a blockchain and automatically sent to insurance providers as proof-of-delivery. You can also use the ledger for general health care management, such as managing healthcare supplies, supervising drugs, regulation compliance, and testing results.

Say Goodbye to Banks and Lawyers?

If you think about a lot of routine financial transactions, what lawyers and banks do boils down to repetitively processing mundane tasks and yet we still have to shell out huge fees for banks to process our mortgage payments or for lawyers to go through wills.

Smart contracts could automate and demystify these processes. This will help ordinary people to save time and money.

When you need mortgage you get it through a bank. However, that bank won’t generally hold onto your mortgage for the entire 30-year loan and your mortgage will be sold to an investor. But you don’t make payments to the investor that owns your mortgage. You keep making payments to the bank and the bank just becomes a processor for your monthly payments. The bank will send a slice to taxes, a chunk to the investor, and a bit for homeowner’s insurance.

“That’s just a real simple operational task. However, to service that mortgage, that bank will often take a quarter to a half percent per year, “says Rapoport. “They’re just doing an operational headache of receiving payments and redirecting them and they’re charging you for that. But it’s something that could theoretically be administered very easily with a smart contract. “

Mortgage processing fees could be eliminated and that savings passed on to consumers if mortgage payments were handled by smart contracts. The result would be a lowered cost of home ownership, which would be great for most people.

Smart contracts have clear potential, although they are still in their nascent stage. If a simple enough user interface were developed it could remove a host of legal headaches. For example, this can help you with updating your will. Imagine if allocating your assets after you die was as simple as moving an adjustable slider that determines who gets what. Just like with the bet or FedEx example, the contract goes into effect and your assets are divvied up once the smart contract can verify the triggering condition–in this case, your death.

It may sound like we won’t need lawyers anymore with all this. But enthusiasts say that smart contracts should not be seen as an erasure of the legal system, but as its evolution.

Thomas says „I don’t think that this will replace the legal system. I think that this will provide an intermediate layer between transacting and going to court. “

Nonetheless, lawyers might have very different role in the future. The role of lawyers might shift to producing smart contract templates on a competitive market rather than having lawyers adjudicate individual contracts. Contract selling points would be their quality, their ease of use, and how customizable they are.

„I think that many people will create contracts that do different things,” says Rapoport. “And they can essentially sell them for others to use, which means that if you make a really good equity agreement that has a bunch of different functionality a company can charge for access to their contract.“

Smart Property and the Internet of Things

It’s easy to think about a smart contract managing a will and if you can imagine yourself keeping all of your assets in bitcoin it all makes sense. But what if you live in the real world and have physical possessions? The answer is something that we call smart property.

Ellis explained that this started to get more sci-fi when we talk about smart property. The so-called “Internet of Things” is constantly growing. It has more and more interconnected devices out there every day and some forward-thinking developers are already working on ways to combine the Internet of Things with bitcoin infrastructure. They want that something like a bitcoin can actually represent a physical object and that token is what these developers call smart property.

These new smart property tokens would actually grant ownership and control to a networked object, whether that be a computer, a car, or even a house. This is more important than representing some object.

Ellis gives the example of renting out his house: “Let’s say all the locks have got network connections, and they are all Internet-enabled. The smart contract you and I agreed to automatically unlocks the house for you when you make a bitcoin transaction for the rent and you just go in using keys stored on your Smartphone.”

A smart contract would also make it trivial to set up dates when those digital keys would automatically expire, which sounds a bit like Airbnb without the need for Airbnb.

And if you think about it, that’s great. That’s the fundamental transformation smart contracts are after. A service like Airbnb obviates the need for the host and the guest to trust each other, and that’s why this service is so desirable. The host and the guest both only need to trust Airbnb. If the host doesn’t leave the keys, or the guest doesn’t pay up, either of them can take it up with Airbnb.

Doing the same sublet with a smart contract would supplant Airbnb’s. The homeowner and renter just need to trust the smart contract and they still don’t need to trust each other. Smart contracts would decentralize the model of who needs to be trusted, which would cut out hefty fees by brokering services like Airbnb.

Smart contracts don’t have to just disrupt existing business models, they can also complement them. Nick Szabo envisioned the idea of smart property writing way back in his ’94 essay. He said that “smart property might be created by embedding smart contracts in physical objects.” His example of choice was a car loan. He said that the smart contract could automatically revoke your digital keys to operate the car if you miss a car payment. Car dealerships would definitely find this appealing.

Smart Contracts are Amazing!

Here’s what smart contracts give you:

Trust – Your documents are encrypted on a shared ledger and there’s no way that someone can say they lost it.

Autonomy – You’re the one making the agreement. This means that there’s no need to rely on a lawyer, broker, or other intermediaries to confirm. Incidentally, since execution is managed automatically by the network, rather than by one or more, possibly biased, individuals who may err, this also knocks out the danger of manipulation by a third party.

Speed – To manually process documents, you’d ordinarily have to spend chunks of time and paperwork. Smart contracts use software code to automate tasks. This feature shaves hours off a range of business processes.

Backup – Imagine if your bank lost your savings account and on the blockchain, each and every one of your friends has your back. This means that your documents are duplicated many times over.

Accuracy – Automated contracts are faster and cheaper. They also avoid the errors that come from manually filling out heaps of forms.

Safety – Cryptography, the encryption of websites, keeps your documents safe, which means that there is no hacking. In fact, to crack the code and infiltrate it would take an abnormally smart hacker.

Savings – Smart contracts knock out the presence of an intermediary, which means that they save you the money. For example, you would have to pay a notary to witness your transaction.

photo (https://blockgeeks.com/wp-content/uploads/2016/10/Smart-Contracts-are-Awesome.png)

Jeff Garzik is an owner of blockchain services Bloq. Here’s how he described smart contracts:

“Smart contracts … guarantee a very, very specific set of outcomes and there’s never any confusion and there’s never any need for litigation.”

This Is Justice for Poor People?

Admittedly, it does start to sound like the makings of a dystopian sci-fi film at some point. Your car could be digitally and remotely repossessed if you can’t make a payment. This would be done without any human interaction.

The upside is that financial institutions should be more willing to take risks on people who might not otherwise get loans. Because, it’s inconsequential for the bank to take back the asset in question if someone can’t pay up. This is the worst case scenario.

Smart contracts also have the potential to open up access to the legal system for disadvantaged people who might not be able to afford it on their own.

In theory the law treats everyone equally. However, you more often than not need money to take someone to court over a breach of contract.

Ellis said that at present justice really only works if you have enough money to hire a lawyer to enforce that agreement. So it will be game-changing once smart contracts have the ability to enforce agreements on their own.

Of course, in reality it may not play out that cleanly. In theory, this all sounds good and noble. However, if a smart contract were ever challenged it’s impossible to predict how it would hold up in court. It is certainly appealing to dethrone lawyers as the high priests of arbitrating contracts. But do we run the risk of just replacing literacy in legalese with literacy in code?

Rapoport admitted that there may be drawbacks and he said that in some ways it’s easier to read a traditional contract because everyone reads in English. But this is still very bleeding-edge technology. This means that we don’t know what kinds of user-facing improvements will be made eventually.

The promise of smart contracts is clear, despite unforeseen pitfalls. We’re waiting to see if either Ethereum or Ripple’s Codius will be able to become usable and really take off.

Ellis said that there are lot of clever people working on this right now. They are high on ideas because they can see the potential. It’s a bit like VHS vs. Betamax because we don’t know who is going to win this race – Ripple or Ethereum.

Now for Issues

Smart contracts are far from perfect and there is a lot to be learned about them. How should these contracts be regulated by governments? What if bugs get in the code? How would these smart contract transactions be taxed by governments? Remember my rental situation as a case in point.

What happens if I send the wrong code? Or, as lawyer Bill Marino points out, I send the right code, but my apartment is condemned before the rental date arrives? I could rescind it in court if this were the traditional contract. However, the blockchain is a different situation and the contract performs, no matter what.

The list of challenges goes on and on and experts are trying to unravel them. But these critical problems do dissuade potential adopters from signing on.

Here’s To the Future of Smart Contracts…

Part of the future of smart contracts lies in entangling these problems. For example, in Cornell Tech there are some lawyers who insist that smart contracts will enter our everyday life. They have dedicated themselves to researching these concerns.

Actually, we’re stepping into a sci-fi screen when it comes to smart contracts. The IT resource center, Search Compliance suggests that smart contracts may impact changes in certain industries, such as law and lawyers will transfer from writing traditional contracts to producing standardized smart contract templates in that case. These templates are similar to the standardized traditional contracts that you’ll find on LegalZoom. Other industries, like credit companies, merchant acquirers, and accountants may also employ smart contracts for tasks. They can employ them as real time auditing and risk assessments. In fact, the website Blockchain Technologies sees smart contracts merging into a hybrid of paper and digital content. Here contracts are verified via blockchain and substantiated by physical copy.

Blockchains Where Smart Contracts Can Be Processed

Bitcoin: Bitcoin is great for processing bitcoin transactions. However, it has limited ability for processing documents.

NXT: NXT is a public blockchain platform. It contains a limited selection of templates for smart contracts. It is important to note that you’re unable to code your own, which means that you have to use what is given.

Side Chains: This is another name for blockchains that run adjacent to Bitcoin. It also offers more scope for processing contracts.

Ethereum: Ethereum is a public blockchain platform. This platform is the most advanced for coding and processing smart contracts and you can code whatever you wish with it. It is important to note that you would have to pay for compute power with “ETH” tokens.

NEO

STRATIS

UBIQ

There’s no end to the range of industries smart contracts can impact, from real estate to law, to healthcare and automobile and the list goes on and on. Gavin Wood, Ethereum CTO, says:

The potential for smart contracts to alter aspects of society is of significant magnitude and this is something that would provide a technical basis for all sorts of social changes. I find that extremely exciting.

Felix Kuester works as an analyst and content manager for Captainaltcoin and specializes in chart analysis and blockchain technology. He is also actively involved in the crypto community - both online as a central contact in the Facebook and Telegram channel of Captainaltcoin and offline as an interviewer he always maintains an ongoing interaction with startups, developers and visionaries. The physicist has couple of years of professional experience as project manager and technological consultant. Felix has for many years been enthusiastic not only about the technological dimension of crypto currencies, but also about the socio-economic vision behind them.